The end of ESG reporting software: why businesses now need an extra-financial ERP

The ESG software market is consolidating. Acquisitions, disappearances, uncertainty: the question is not which tools will survive. The real question is what replaces them. The answer: the extra-financial ERP.

Temps de lecture estimé : X min

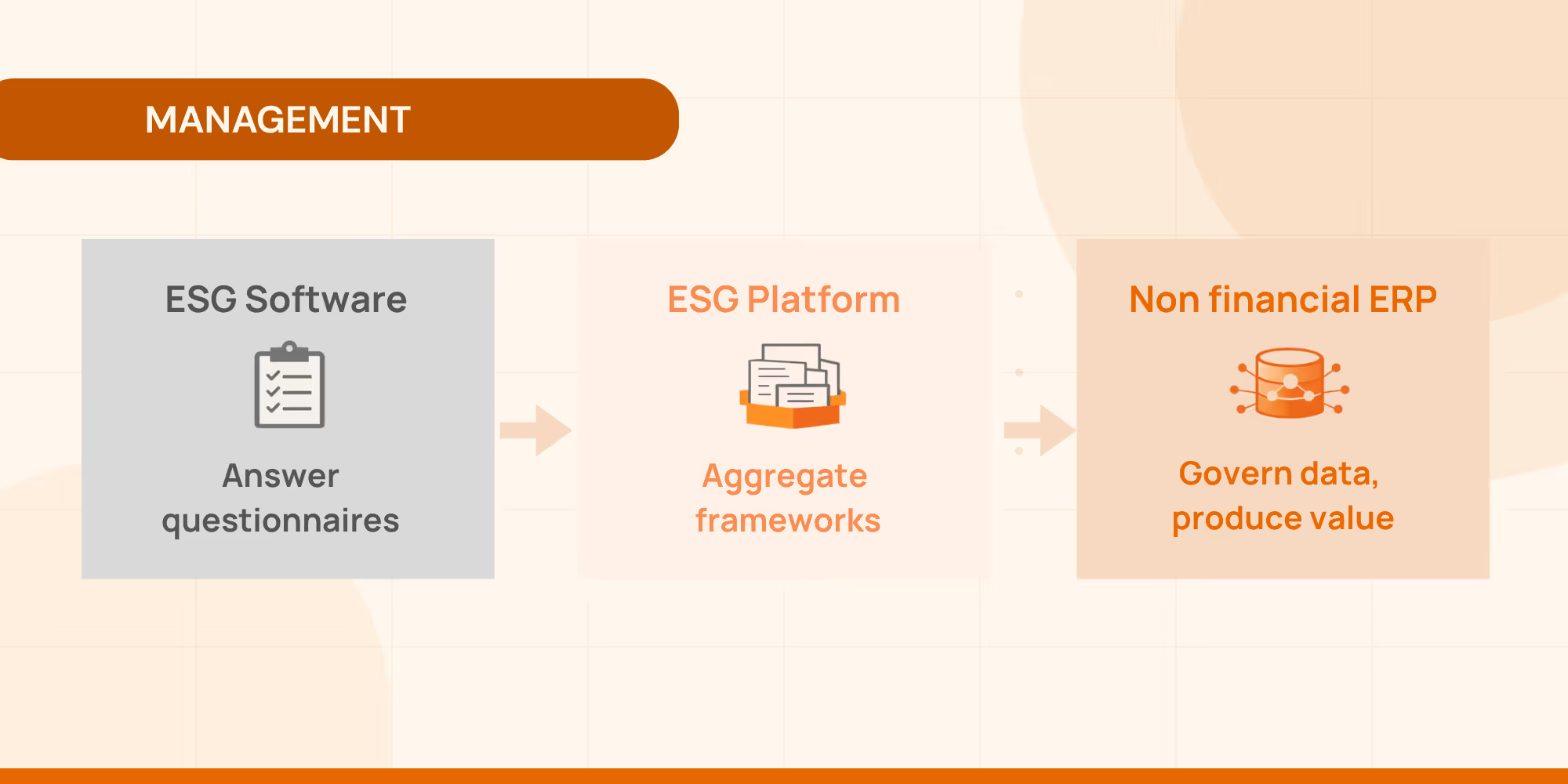

The first generation: ESG reporting software

The first generation of ESG tools developed around a simple need: facilitate reporting.

Faced with the multiplication of frameworks and questionnaires, companies had to answer:

- regulatory frameworks (CSRD, Taxonomy, etc.)

- voluntary standards (GRI, TCFD...)

- questionnaires from investors or rating agencies (EcoVadis, CDP...)

- customer requests or any other stakeholder in the value chain

ESG software therefore provided an initial response: centralizing responses, structuring collection and facilitating reporting. This approach is still useful. But it is based on a logic that is now showing its limits: The logic of the questionnaire.

In this model, companies respond to a succession of external requests, each with its own format and structure. The extra-financial data is then produced in response to requests, and not as a strategic business asset.

The second step: the multiplication of reference frames of reference

To adapt to this growing complexity, publishers have developed solutions multi-referential in order to allow companies to respond to several frameworks from the same information base. A logical evolution, but which still remains in a logic of Reporting.

It is incomplete. Because businesses need to go further:

- produce trackable data

- document their methodologies

- pilot action plans

- monitor the evolution of their risks and opportunities

- connect this information with strategy and finance

It's not just about knowing How to respond to a framework But to know how to govern the company's extra-financial data over time.

The switch to data governance

This change is largely due to CSRD. Even though its scope has recently evolved, it has established two structuring principles: double materiality and auditing. These requirements are profoundly transforming the role of extra-financial data.

It is no longer a simple statement. It gradually becomes:

- traceable

- Documented

- audited

- Comparative

- used in strategic decisions and in operational performance management.

This movement progressively brings extra-financial data closer to financial data. However, businesses already have a system for managing financial data: The ERP.

An ERP organizes the collection, traceability, controls, audit and management of information. The same logic is starting to apply to extra-financial data today.

Extra-financial ERP: a data infrastructure

Unlike traditional ESG software, an extra-financial ERP is not limited to reporting. It acts like an infrastructure for managing extra-financial data.

Its role is to enable businesses to:

- structure their data

- document their methods

- organize collection processes`

- govern responsibilities

- follow the action plans

- and connect this information to strategic decisions.

In this architecture, the repositories no longer constitute the core of the system. They become A layer of interpretation.

The company produces structured and governed data at the source, which becomes The reference system for extra-financial data within the organization. This data can then be used to meet various uses:

- regulatory reporting

- Investor quizzes

- risk analysis

- strategic management

- access to finance.

Extra-financial data then ceases to be an administrative constraint to become a strategic asset.

An evolution driven by finance and risks

Another factor is accelerating this transformation: the increasing integration of extra-financial considerations into risk assessment.

Banks, insurers and investors are increasingly relying on this information to analyze:

- business resilience

- their exposure to climate risks

- the robustness of their value chain

- their critical dependencies

In some strategic sectors, this dimension is becoming even more visible.

In the defence industry, for example, access to finance increasingly depends on the ability of companies to document:

- their industrial dependencies

- their energy resilience

- their geopolitical risks

- their risk governance.

The real challenge: transforming data into capital

The current evolution of the ESG market should therefore not be interpreted only as a consolidation of players. It reflects a deeper transformation.

Businesses are gradually moving from a logic where they produce responses To a logic where they manage a wealth of extra-financial data.

In this new data economy, the tools that can survive will not only be those that aggregate repositories.

They will be the ones that allow businesses to:

- produce reliable data

- Govern it over time

- share it with their stakeholders

- and use it to manage their strategic, financial and operational decisions.

In other words, extra-financial data becomes capital. And like any capital, it requires infrastructure to be managed.

This is precisely the role that extra-financial ERPs are called to play in the years to come.